Cleveland DSCR loans qualify on the property's rental cash flow — not W-2, not tax returns. Median $130K SFR · $1,225 rent · 0.94% R/P · 5 GREEN-list neighborhoods. Why Cleveland became America's #1 DSCR market. Cleveland's rent-to-price math, working-class demand pools, and DSCR underwriting let investors close in roughly two weeks through Homestead Capital.

Cleveland Hot Minute · 2026-05-15

The 30-second case

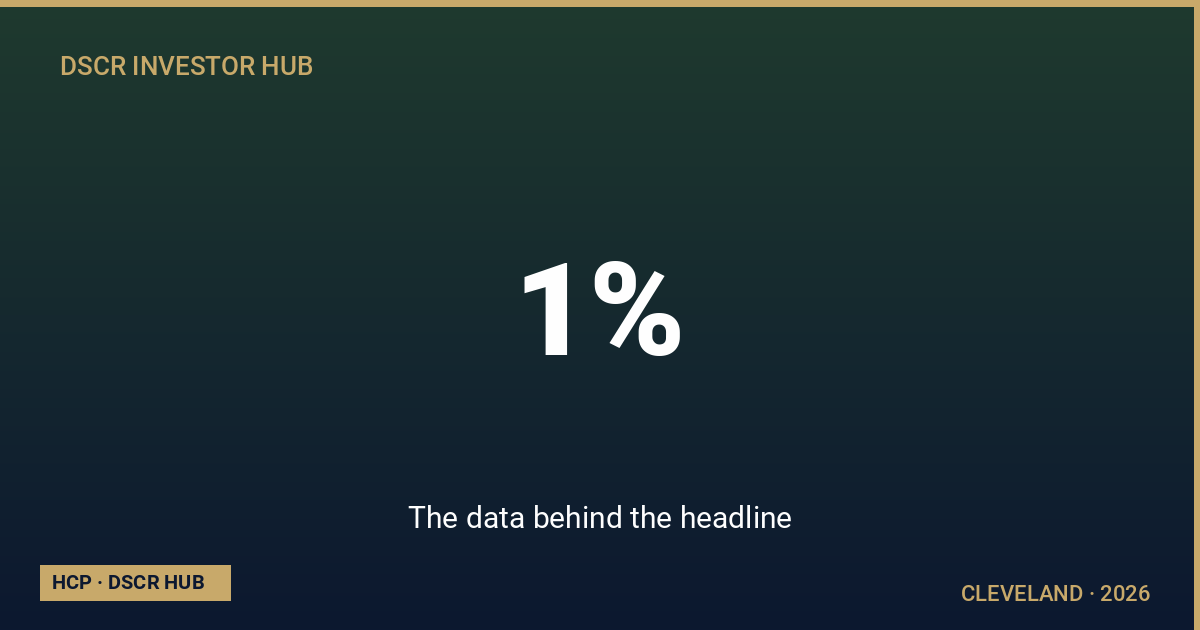

Cleveland is the cleanest DSCR math in the United States in 2026. Median single-family home: $130K. Median rent: $1,225/mo. That's a 0.94% rent-to-price ratio — better than any top-15 US metro and well past the traditional 1% rule when you concentrate buying inside the five working-class neighborhoods below.

Cleveland Clinic, University Hospitals, Sherwin-Williams, and KeyCorp anchor a recession-resilient employment base. Cuyahoga County's 2% property tax is the only drag, and it disappears once rent-to-price climbs into the target zones. DSCR underwriting reads the property's rent — not your W-2, not your tax returns.

The data behind the headline

The 1% rule — the old investor heuristic that says monthly rent should equal 1% of purchase price — has been broken in coastal metros for a decade. Cleveland is one of a small group of Midwest metros that not only meets the 1% rule at the neighborhood level but exceeds it.

Why this beats the traditional 1% rule: at the neighborhood level, Cleveland clears 1.0–1.6% R/P. The metro number is dragged down by the appreciation-driven west-side districts (Tremont, Ohio City proper) where prices have outrun rents. When you sort the city by zip code and apply the DSCR feasibility screen, the working-class submarkets pencil DSCR ratios of 1.30 to 1.65 at 80% LTV — well clear of the 1.0 break-even threshold most DSCR programs require.

Rent growth ran 4.6% YoY through Q1 2026 (Zillow ZORI) — second nationally only to Memphis. Vacancy sits at 6.9% (BLS Cleveland-Elyria MSA). The tenant base is healthcare, hospital, insurance, and education — wage segments that don't flinch in recession.

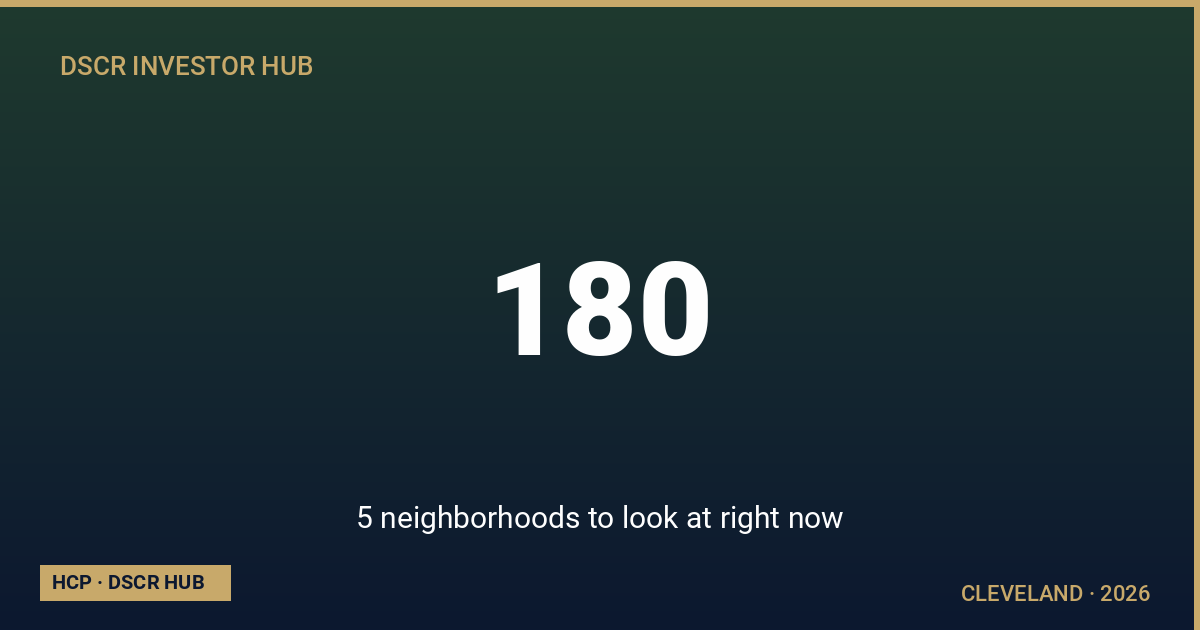

5 neighborhoods to look at right now

From task #180's DSCR feasibility validation report (2026 Q1), these are the GREEN-list Cleveland neighborhoods — submarkets where the cash-flow math, comp depth, and Section-8 voucher density all stack favorably for a portfolio scaler. Each is ranked by DSCR feasibility score (1–10, higher = better).

1. Glenville (44108)

East side · workforce SFR + duplex

- Feasibility

- 9.2 / 10

- Price band

- $75K–$120K

- Rent band

- $1,000–$1,250

- Implied DSCR

- 1.40–1.65

- Archetype

- Brick rowhouse + workforce SFR

- Section-8

- Deep voucher pool

Cleveland's highest cashflow zone — east side. Working-class tenant base, strong CMHA voucher absorption, replacement comps in the same band keep the rent floor defensible.

2. Slavic Village (44105)

South-east · SFR + small duplex

- Feasibility

- 9.0 / 10

- Price band

- $70K–$115K

- Rent band

- $950–$1,200

- Implied DSCR

- 1.40–1.65

- Archetype

- Working-class SFR + duplex

- Section-8

- Deep voucher pool

17.7% gross yield on the lower end of the band (Sept 2025 data). Deepest replacement tenant pool in the metro thanks to CMHA voucher allocations. Active property management required.

3. Buckeye-Shaker (44120)

Inner-ring east · stabilized walkable

- Feasibility

- 8.8 / 10

- Price band

- $105K–$155K

- Rent band

- $1,150–$1,400

- Implied DSCR

- 1.30–1.55

- Archetype

- Inner-ring SFR + duplex

- Section-8

- Moderate voucher pool

Walkable, stabilized, with University Circle and Shaker Square commute proximity. First-deal-friendly — rent + comp combination minimizes friction for an investor new to Cleveland.

4. Old Brooklyn (44109)

West side · stable workforce SFR

- Feasibility

- 8.6 / 10

- Price band

- $115K–$165K

- Rent band

- $1,200–$1,450

- Implied DSCR

- 1.30–1.50

- Archetype

- Bungalow + workforce SFR

- Section-8

- Light–moderate

West-side bungalow corridor with a more market-rate tenant profile than the east-side zones. Lower management overhead. Comps are deep — appraisals are easy to defend.

5. Lee-Harvard (44128)

South-east · stabilized workforce SFR

- Feasibility

- 8.4 / 10

- Price band

- $95K–$140K

- Rent band

- $1,100–$1,350

- Implied DSCR

- 1.30–1.50

- Archetype

- Post-war ranch + workforce SFR

- Section-8

- Moderate voucher pool

One of the more stable owner-occupied southeast zones with a tenant profile mixing Section-8 and market-rate workforce. Cap rates stay defensible on a 6-year hold.

Property data above is a screening estimate, not a credit offer. DSCR ranges modeled at 80% LTV, 30-year term, illustrative-only rate assumption. Final qualifying DSCR is determined by appraisal, county tax assessor PITIA, and underwriter review.

Cuyahoga County's 2% property tax — why it's not the deal-killer it looks like

- • Investors who haven't underwritten Cleveland see "2% effective property tax" and back away.

- • That instinct is wrong for one reason: the tax is paid on the assessed value (which usually trails market price by…

- • Even at the headline 2.2% tax rate, the rent-to-price ratio overwhelms the drag.

- • Compare this to a Birmingham property at 0.4% tax — same purchase price, same rent, the DSCR comes in at…

- • The Cleveland tax penalty costs you about 0.15 DSCR.

- • Translation: the 2% tax is real but it does not kill the deal. Underwrite the actual parcel's tax bill…

DSCR loan terms for Cleveland investors

Homestead Capital Partners originates Cleveland DSCR loans through the UWM Blueprint program. Core terms — verified against UWM and jhoward Knowledge article 104 as of the most recent weekly audit:

Qualification basis

Property DSCR ≥ 1.0 — the property's rent covers PITIA. No W-2, no tax returns, no employment verification.

LTV

Up to 80% on purchase. Up to 75% on cash-out refinance.

FICO minimum

620 minimum; meaningful pricing tiers at 680, 720, and 760+.

Property types

1–4 unit residential investment. Long-term and short-term rental both qualify where zoning permits.

Close in LLC

Yes — single-member, multi-member, and Series LLC structures all accepted.

Cash-out reserves

Cash-out refinance proceeds may count toward post-close reserve requirements.

Specific rates, payments, and down-payment percentages are Regulation Z trigger terms and require full APR disclosure when combined. Talk to a licensed loan officer for current pricing.

What this means for the typical DSCR investor

Cleveland penciles three distinct investor archetypes — each with a slightly different play. Match yourself to the closest archetype before you start scouting.

Archetype 1 — The workforce-SFR scaler

You're acquiring 3–10 doors per year, $80K–$140K each, mostly Glenville, Slavic Village, and Lee-Harvard. Target $200–$350 monthly cashflow per door after PITIA, maintenance reserve, and PM fee. Cleveland lets you stack faster than any Tier-1 metro because entry prices are low and rents are high. Section-8 voucher acceptance accelerates lease-up. DSCR underwriting on each property means you close in your LLC without your DTI killing the next deal.

Archetype 2 — The BRRRR investor

You buy in cash or with private money, rehab to a $1,250–$1,400 rent point, season for 6 months, then DSCR-refinance at up to 75% LTV cash-out. Buckeye-Shaker and Old Brooklyn are the strongest BRRRR submarkets because comp depth makes the appraisal defensible. Textbook play: buy at $85K, put in $35K of rehab, appraise at $155K, pull $116K cash out, leave $20K of forced equity behind.

Archetype 3 — The out-of-state portfolio holder

You live in California, Texas, or the Northeast. You want geographic diversification plus cashflow you can't get at home. Cleveland is the standard out-of-state safe pick because property management infrastructure is mature, title work is clean, and the tenant base is stable. DSCR loans let you keep stacking even when your W-2 lender says you're maxed at 10 financed properties. Start in Buckeye-Shaker or Old Brooklyn.

Common questions

DSCR underwriting qualifies the property, not you. The lender wants the subject-property lease (or appraiser-supported market-rent comp), Cuyahoga County tax + insurance estimate, two months of bank reserves, and generally 620+ FICO. No tax returns, no employer verification. Clean files close in 21–30 days.

DSCR loans don't fund rehab directly — they're for stabilized rentals. Standard BRRRR path: buy in cash or with a short-term lender, rehab, season for 6 months, then DSCR-refinance at up to 75% LTV cash-out. Your loan officer can coordinate the bridge-to-DSCR sequence so the refi closes the day seasoning hits.

Yes, where local zoning and ordinances permit. Cleveland-proper STR regulations are evolving — check the city's current rental registration rules before underwriting an STR-only thesis. For DSCR purposes, STR income qualifies when supported by a 12-month operating history or a market-rent analysis from the appraiser (Form 1007 / 1025 + AirDNA-style comp).

The market has 8–10 mid-sized PM firms that specialize in workforce SFR portfolios. Typical fee structure is 8–10% of monthly rent plus a one-month placement fee. Section-8 specialists charge slightly more but absorb the CMHA paperwork. Ask your loan officer for a current vetted PM list before you close.

No. Section 8 is treated equivalently to market-rate rent. Qualifying income is the lower of the contracted voucher amount and the appraiser-supported market rent. Many Cleveland investors run mixed portfolios — Section-8 in higher-yield east-side zones, market-rate in the west-side bungalow corridor.

Three common exits: DSCR cash-out refi to recycle equity into more doors; 1031 exchange into a Sun Belt market (Memphis or Birmingham are common parallels) once Cleveland equity matures; or sale to a regional multifamily aggregator if you've consolidated 25+ doors in a single submarket. Cleveland's transactional market is liquid in the $80K–$200K SFR band.

Get your free Cleveland DSCR market analysis

15-minute walkthrough of the property, the neighborhood, and the qualifying DSCR. No income docs. No commitment.

Property illustration disclaimer. Property shown for illustrative purposes only. Actual loan amounts depend on appraised value, borrower qualifications, and program rates. Neighborhood price and rent bands above are screening estimates compiled from publicly available 2026 Q1 data and are not a representation, warranty, or commitment to lend on any specific parcel. Per 24 CFR § 109.30.

Homestead Capital Partners · NMLS #2587985 · originated by Homestead Capital Partners. NEXA Mortgage, LLC (DBA NEXA Lending) · NMLS #1660690 · Equal Housing Lender. 5559 S Sossaman Rd Bldg #1 Ste #101, Mesa, AZ 85212.

State licensure verified at nmlsconsumeraccess.org. DSCR loans are business-purpose loans for real-estate investors, not consumer-purpose loans. Information presented is for educational purposes and does not constitute a commitment to lend. Loan programs and terms are subject to change without notice. Not all applicants will qualify. Subject to credit and underwriting approval.

Related DSCR markets & sources

Compare this market against the rest of the Homestead Capital DSCR coverage map, or jump to the underlying data sources cited above.

Sibling DSCR markets

- Detroit DSCR tipping point analysis

- Memphis DSCR cash-flow market

- Cleveland DSCR neighborhood feasibility scores

DSCR loan fundamentals

Authoritative external sources

- verify NEXA Mortgage NMLS #1660690 — Always verify your lender on NMLS Consumer Access before signing — DSCR loans are originated through NEXA Mortgage.

- Zillow Research ZHVI and ZORI data — Independent home-value (ZHVI) and rent-index (ZORI) data are published monthly by Zillow Research and are the basis for the price and rent figures cited above.

DSCR Markets — sibling cities

Compare this market against the rest of the Homestead Capital DSCR coverage map. Each city uses the same methodology and source set so the math is directly comparable.